The UK will be leaving the EU on 29 March 2019. Leaving the EU with a deal remains the Government’s top priority, however the government and businesses should continue to plan for every possible outcome including no deal.

In December, HMRC wrote to VAT-registered businesses that trade only with the EU advising them to take 3 actions to prepare for a no deal EU Exit, including registering for an UK Economic Operator Registration and Identification (EORI) number. You can read the full letter here.

Businesses that only trade with the EU will need an EORI number:

to continue to import or export goods with the EU after 29 March 2019, if the UK leaves the EU without a deal; and

before they can apply for authorisations that will make customs processes easier.

If you are a UK business that trades with the EU and do not already have an EORI number then you should register for an EORI number at GOV.UK now. It only takes 10 minutes to apply. These businesses should also decide if they want to hire an agent to make import and/or export declarations for them or make the declarations themselves.

We will continue to support businesses in their preparations for leaving the EU, including registering for an EORI number, as the 29 March 2019 approaches.

HMRC is phasing in its landmark Making Tax Digital (MTD) regime, which will ultimately require taxpayers to move to a fully digital tax system. Regulations have now been issued which set out the requirements for MTD for VAT. Under the new rules, businesses with a turnover above the VAT threshold (currently £85,000) must keep digital records for VAT purposes and provide their VAT return information to HMRC using MTD functional compatible software.

The new rules have effect from 1 April 2019 where a taxpayer has a ‘prescribed accounting period’ which begins on that date, or otherwise from the first day of a taxpayer’s first prescribed accounting period beginning after 1 April 2019. HMRC has recently announced that the rules will have effect for some VAT-registered businesses with more complex requirements from 1 October 2019. Included in the deferred start date category are VAT divisions, VAT groups and businesses using the annual accounting scheme.

HMRC has recently opened a pilot service for businesses with straightforward affairs and the pilot scheme will be gradually extended for other businesses in the next few months.

Keeping digital records and making quarterly updates will not be mandatory for taxes other than VAT before April 2020.

Keeping digital records will not mean businesses are mandated to use digital invoices and receipts but the actual recording of supplies made and received must be digital. It is likely that third party commercial software will be required. Software will not be available from HMRC. The use of spreadsheets will be allowed, but they will have to be combined with add-on software to meet HMRC’s requirements.

In the long run, HMRC is still looking to a scenario where income tax updates are made quarterly and digitally, and this is really what the VAT provisions anticipate.

Corporation tax rates

Corporation tax rates have already been enacted for periods up to 31 March 2021.

The main rate of corporation tax is currently 19% and will remain at this rate for next year. The rate will fall to 17% for the Financial Year beginning on 1 April 2020.

Class 2 and 4 National Insurance contributions (NICs)

The government has recently announced that Class 2 NICs will not be abolished for the duration of this Parliament. The Chancellor confirmed in March 2017 that there will be no increases to Class 4 NICs rates in this Parliament.

UK property income of non-UK resident companies

Changes are made for non-UK resident companies that carry on a UK property business either directly or indirectly, for example through a partnership or a transparent collective investment vehicle.

Following consultation, from 6 April 2020, non-UK resident companies that carry on a UK property business, or have other UK property income, will be charged to corporation tax, rather than being charged to income tax as at present.

Capital allowances

Annual Investment Allowance

The government has announced an increase in the Annual Investment Allowance for two years to £1 million in relation to qualifying expenditure incurred from 1 January 2019. Complex calculations may apply to accounting periods which straddle this date.

Other changes

A number of changes are made to other rules relating to capital allowances:

a reduction in the rate of writing down allowance on the special rate pool of plant and machinery, including long-life assets, thermal insulation, integral features and expenditure on cars with CO2emissions of more than 110g/km, from 8% to 6% from April 2019. Complex calculations may apply to accounting periods which straddle this date

clarification as to precisely which costs of altering land for the purposes of installing qualifying plant or machinery qualify for capital allowances, for claims on or after 29 October 2018

the end of the 100% first year allowance and first year tax credits for products on the Energy Technology List and Water Technology List from April 2020

an extension of the current 100% first year allowance for expenditure incurred on electric charge-point equipment until 2023.

In addition, a new capital allowances regime will be introduced for structures and buildings. It will be known as the Structures and Buildings Allowance and will apply to new non-residential structures and buildings. Relief will be provided on eligible construction costs incurred on or after 29 October 2018, at an annual rate of 2% on a straight-line basis.

Change to the definition of permanent establishment

A non-resident company is liable to corporation tax only if it has a permanent establishment in the UK. Certain preparatory or auxiliary activities, such as storing the company’s own products, purchasing goods or collecting information for the non-resident company, are classed as not creating a permanent establishment.

From 1 January 2019, the exemption will be denied to these activities if they are part of a ‘fragmented business operation’.

Preventing abuse of the R&D tax relief for SMEs

To help prevent abuse of the Research and Development (R&D) SME tax relief by artificial corporate structures, the amount that a loss-making company can receive in R&D tax credits will be capped at three times its total PAYE and NICs liability from April 2020.

Protecting taxes in insolvency

From April 2020, HMRC will have greater priority to recover taxes paid by employees and customers.

The changes appear to be mainly targeted at the distribution of funds to financial institutions as creditors. The rules will remain unchanged for taxes owed by the business and HMRC will remain below other preferential creditors such as the Redundancy Payment Service.

Other measures

Changes to the tax treatment of corporate capital losses from 1 April 2020 to restrict the proportion of annual capital gains that can be relieved by brought-forward capital losses to 50%.

Changes to the Diverted Profits Tax from 29 October 2018.

An increase in the small trading tax exemption limits for charities from April 2019 from £5,000 per annum or, if the turnover is greater than £5,000, 25% of the charity’s total incoming resources, subject to an overall upper limit of £50,000, to £8,000 and £80,000 respectively.

The introduction of an income tax charge to amounts received in a low tax jurisdiction in respect of intangible property, to the extent that those amounts are referable to the sale of goods or services in the UK, from 6 April 2019, with targeted anti-avoidance rules for arrangements entered into on or after 29 October 2018.

Digital Services Tax

The government remains committed to reform of the international corporate tax framework for digital businesses. However, pending global reform, interim action is needed to ensure the corporate tax system is sustainable and fair across different types of businesses.

Therefore, the government has announced that it will introduce a Digital Services Tax (DST) which will raise £1.5 billion over four years from April 2020. The DST will apply a 2% tax on the revenues of search engines, social media platforms and online marketplaces where their revenues are linked to the participation of UK users.

Businesses will need to generate revenues of at least £500 million globally to become taxable under the DST. The first £25 million of relevant UK revenues are also not taxable.

Intangible fixed assets

The Intangible Fixed Assets regime, which was introduced from 1 April 2002, fundamentally changed the way the UK corporation tax system treats intangible fixed assets (such as copyrights, patents and goodwill). As the regime is now more than 15 years old, the government would like to examine whether there is scope for reforms that would simplify it and make it more effective in supporting economic growth.

Following a short consultation, the government will seek to introduce targeted relief for the cost of goodwill in the acquisition of businesses with eligible intellectual property from April 2019.

With effect from 7 November 2018, the government will also reform the de-grouping charge rules, which apply when a group sells a company that owns intangibles, so that they more closely align with the equivalent rules elsewhere in the tax code.

VAT registration limits

The government had previously announced that the VAT registration and deregistration thresholds would be frozen at £85,000 and £83,000 respectively until April 2020.

The government has now announced that this freeze will continue for a further two years from 1 April 2020.

VAT fraud in labour provision in the construction sector

The government will pursue legislation to shift responsibility for paying VAT along the supply chain with the introduction of a domestic VAT reverse charge for supplies of construction services with effect from 1 October 2019. The long lead-in time reflects the government’s commitment to give businesses adequate time to prepare for the changes.

VAT treatment of vouchers

Draft legislation has been issued to insert a new tax code for the VAT treatment of vouchers, such as gift cards, for which a payment has been made and which will be used to buy something. The legislation separates vouchers with a single purpose (eg a traditional book token) from the more complex gift vouchers and sets out how and when VAT should be accounted for in each case. The new legislation is not concerned with the scope of VAT and whether VAT is due, but with the question of when VAT is due and, in the case of multi-purpose vouchers, the consideration upon which any VAT is payable.

VAT collection – split payment

The government wants to combat online VAT fraud by harnessing new technology and is consulting on VAT split payment. This will utilise payments industry technology to collect VAT on online sales and transfer it directly to HMRC. In the government’s view this would significantly reduce the challenge of enforcing online seller compliance and offer a simplification for business.

If you run a VAT-registered business with a taxable turnover above the VAT registration threshold (currently £85,000) you are required to keep digital VAT business records and send returns using Making Tax Digital (MTD)-compatible software for VAT periods starting on or after 1 April 2019. Businesses with a taxable turnover below the VATthreshold can also sign up for MTD for VAT voluntarily. This also applies to other VATentities, such as charities, government bodies and limited companies.

The MTD for VAT pilot started in April 2018 and is currently in a private stage, available only to invited volunteer VAT businesses and their agents. This is so we can work with software providers, testing our systems and their products on a small scale before opening MTD to a wider audience. At the moment we are limiting the number and types of business we invite into the pilot. We’ll provide more guidance about how to sign up to MTD for VAT on GOV.UK later in the year, but you can email us if you are interested in becoming involved in the private VAT pilot earlier.

If you have an agent, you should speak to them to find out when it may be best for you to join the pilot.

When MTD for VAT will be mandatory for your business

If you are registered for VAT and your taxable turnover is above the VAT registration threshold (currently £85,000), for accounting periods starting on or after 1 April 2019, you must keep digital business records and send your VAT returns to HMRC using MTD-compatible software.

If your taxable turnover drops below the VAT registration threshold at any point after 1 April 2019 you are still required to continue to keep digital records and send HMRCyour VAT returns using MTD-compatible software. This obligation doesn’t apply if you de-register from VAT or if you are exempt from MTD for VAT.

What happens if your taxable VAT turnover is below the VAT MTD threshold

If your business has a taxable turnover below the VAT threshold you can still sign up for MTD voluntarily. HMRC is encouraging businesses with a taxable turnover below the VAT threshold to sign up so they can also benefit from MTD. Businesses can also sign up for MTD for Income Tax. This means, subject to your business type, you can further streamline your business processes. You can read more about MTD for Income Tax further down.

Software will help you stay on top of business record keeping, allowing you (and your agent, if you have one) to better understand how your business is performing.

What your business needs to do to be ready to sign up for MTD

You will need to keep your business records digitally from the start of your accounting period. If you already use software to keep your business records, check your software provider’s plans to introduce MTD-compatible software.

If you don’t currently use software, or your software won’t be MTD-compatible, you’ll need to consider what software is suitable for your requirements.

We’ll publish details of the VAT software available later in the year, when we open the VAT pilot to more businesses. Read about software providers currently supporting MTDfor VAT.

Using spreadsheets for your business records

A spreadsheet can be used to calculate or summarise VAT transactions to arrive at the return information you need to send HMRC.

If you use spreadsheets to keep business records, you’ll need MTD-compatible software so that you can send HMRC your VAT returns and receive information back from HMRC. Bridging software may be required to make spreadsheets MTD-compatible. You can read what we mean by ‘bridging software’ below.

The information must not be physically re-typed into another software package.

Records that you need to keep digitally for MTD for VAT

MTD does not require you to keep additional records for VAT, but to record them digitally.

Your digital records should include, for each supply, the time of supply (tax point), the value of the supply (net excluding VAT) and the rate of VAT charged. They should also include information about your business, including business name and principle business address, as well as your VAT registration number and details of any VATaccounting schemes you use.

MTD-compatible software

Compatible software is a software product or set of software products that between them support the MTD obligations of keeping digital records and exchanging data digitally with HMRC through the MTD service. If more than one application is being used, data that flows between those applications must also be exchanged digitally.

Digital records can be kept in a range of compatible digital formats. They do not all have to be held in the same place or on one piece of software. For example, a spreadsheet can be a component of digital record keeping provided the product that consolidates records, or summary records from the spreadsheet, can exchange data digitally with HMRC.

HMRC will give businesses until 31 March 2020 to make sure there are digital links between software products. Before that date, cut and paste will be an acceptable way to transfer information.

The exception to this is where return information is to be transferred to a software product enabled for an Application Programming Interface (an API provides a secure link between software and HMRC) and designed to submit the 9-box VAT return (such as bridging software). In those circumstances the transfer of information must only be digital.

If in doubt, businesses should discuss with their agent or software provider.

Bridging software

‘Bridging software’ is HMRC’s description of the digital tool that can take information from other applications, for example, a spreadsheet or an in-house record keeping system, and lets the user send the required information digitally to HMRC in the correct format.

This notice provides information further to the provisions of The Value Added Tax (Amendment) Regulations 2018 (SI 2018 No. 261), which amend the VAT Regulations 1995 (‘the regulations’).

Parts of this notice include rules that have the force of law under the regulations. These rules are indicated by being placed in a box. Unless otherwise indicated within the rule, all of the rules contained in this Notice have the force of law from the date the regulations have the force of law.

1 Introduction

1.1 What this notice is about

This notice gives guidance on the digital record keeping and return requirements for Making Tax Digital for VAT. This notice is not a standalone document and should be read in conjunction with other VAT notices, in particular the ones listed at paragraph 1.3below. These are all available on GOV.UK.

1.2 Making Tax Digital explained

Making Tax Digital for VAT requires VAT registered businesses with taxable turnover above the VAT registration threshold to keep records in digital form and file their VAT Returns using software.

It is increasingly common for business records and accounts to be kept digitally, in a software program on a computer or tablet, or in a smartphone application, or maintained through such a device and stored using a cloud-based application. The difference under Making Tax Digital is that the software which businesses use must be capable of keeping and maintaining the records specified in the regulations, preparing their VAT Returns using the information maintained in those digital records and communicating with HMRC digitally via our Application Programming Interface (API) platform.

If your digital records are up to date, software will be able to collate and prepare your return for you. It will then show the return to you and ask you to declare that it is correct and confirm that you want to submit it to HMRC. Once you have submitted your return you will receive confirmation through your software that it has been received.

This notice provides further details of the Making Tax Digital rules.

1.3 Other helpful notices

You may find it helpful to read these notices on related subjects:

Make sure you have read the notices relevant to your circumstances before you submit your VAT Return.

2 Check if you have to follow the Making Tax Digital rules

2.1 Turnover test (exemption on the grounds of taxable turnover)

With effect from 1 April 2019, if your taxable turnover is above the VAT registration threshold you must follow the rules set out in this notice. If your taxable turnover subsequently falls below the threshold you will need to continue to follow the Making Tax Digital rules, unless you deregister from VAT or meet other exemption criteria (see paragraph 2.2 of this notice).

Only businesses with taxable turnover that has never exceeded the VAT registration threshold (currently £85,000) will be exempt from Making Tax Digital. You will therefore need to keep an eye on your taxable turnover, especially if you think it is close to the VAT registration threshold.

VAT taxable turnover is the total value of everything you sell that is not exempt from VAT. VAT Notice 700/1: should I be registered for VAT provides more information on the VAT registration threshold and taxable turnover.

2.1 .1 Find out when the Making Tax Digital rules start

The Making Tax Digital rules apply from your first VAT period starting on or after 1 April 2019. A ‘VAT period’ is the inclusive dates covered by your VAT Return.

Example 1 – Existing business with taxable turnover above the VAT registration threshold on 1 April 2019

A business submits a quarterly return covering the period 1 March to 31 May 2019. The business taxable turnover exceeds the VAT registration threshold and therefore the business will need to comply with Making Tax Digital rules for the period starting 1 June 2019.

Example 2 – Business with a taxable turnover above the Making Tax Digital threshold at the point they need to register for VAT

A business that is not registered for VAT is required to register from September 2019 because the taxable turnover over the previous 12 months has exceeded the VAT registration threshold. The business must follow the rules in this notice for all VAT Returns they are subsequently required to make as their taxable turnover was above the VAT threshold when they were required to register.

Example 3 – VAT registered business with taxable turnover below Making Tax Digital threshold until November 2019

A business is registered for VAT but its taxable turnover is below the VAT registration threshold until November 2019. The business must follow the rules in this notice for any VAT period that starts on or after 1 December 2019 as its taxable turnover now exceeds the VAT registration threshold.

2.2 Other exemptions

You will not have to follow the Making Tax Digital rules where HMRC is satisfied that:

your business is run entirely by practicing members of a religious society whose beliefs are incompatible with the requirements of the regulations (for example, those religious beliefs prevent them from using computers)

it is not reasonably practicable for you to use digital tools to keep your business records or submit your returns, for reasons of age, disability, remoteness of location or for any other reason

you are subject to an insolvency procedure

These may apply even if you are not currently exempt from online filing for VAT.

If you think any of these apply to you then contact the VAT Helpline to discuss alternative arrangements. If HMRC consider that an exemption is not appropriate, digital assistance may be available to help you get online support.

2.3 How you can choose not to be exempt from the rules

If you are exempt from Making Tax Digital you may still choose to follow the Making Tax Digital rules.

To do this, you must tell HMRC before the start of the next VAT period that you want to use the Making Tax Digital service and also the date that your next VAT period begins. You will then be subject to the Making Tax Digital rules from the start of that next VAT period.

You may decide, for a later period, that you no longer wish to follow the Making Tax Digital rules. If you are still exempt from Making Tax Digital at that point, you can tell HMRC you want to leave the Making Tax Digital service and submit returns the way you submitted them before you chose to follow the Making Tax Digital rules. This will be from the start of the next VAT period following the date you told us.

You must tell HMRC in writing if you want to join or leave Making Tax Digital.

3 Digital record-keeping

3.1 Digital record-keeping

All VAT registered businesses must keep and preserve certain records and accounts. Under Making Tax Digital, some of these records (see paragraph 3.3) must be kept digitally within functional compatible software (see paragraph 3.2). Records that are not specified in this notice, or that are not required to complete your VAT Return, do not need to be kept in functional compatible software.

Some software will record all your VAT records and accounts information. However, there are some records that by law must be kept and preserved in their original form either for VAT purposes or other tax purposes. For example you must still keep a C79 (import VAT certificate) in its original form.

Example 1

A business receives an invoice and types selected data contained in the invoice into functional compatible software. They must still keep the invoice in its original form as the data in the functional compatible software is not a copy of the invoice.

Example 2

A business has functional compatible software that scans the invoices received and puts the information in its ledger. If the image is retained and contains all the detail required for VAT purposes then the business does not need to keep the original invoice unless it is required for another purpose.

If you deregister from VAT you will no longer need to keep digital records in functional compatible software, but you must retain your VAT records for the required period.

provide to HMRC information and returns from data held in those digital records by using the API platform

receive information from HMRC via the API platform

HMRC expects that there will be software products available that will perform all of the functions listed above. Some software programs will not be able to perform all of these functions by themselves. For example, a spreadsheet or other software product that is capable of recording and preserving digital records may not be able to perform the other 2 functions listed above, but can still be a component of functional compatible software if it is used in conjunction with one or more programs that do perform those functions.

The complete set of digital records to meet Making Tax Digital requirements does not all have to be held in one place or in one program. Digital records can be kept in a range of compatible digital formats. Taken together, these form the digital records for the VAT registered entity.

3.2 .1 Digital links

Data transfer or exchange within and between software programs, applications or products that make up functional compatible software must be digital where the information continues to form part of the digital records. Once data has been entered into software used to keep and maintain digital records, any further transfer, recapture or modification of that data must be done using digital links. Each piece of software must be digitally linked to other pieces of software to create the digital journey.

It follows that transferring data manually within or between different parts of a set of software programs, products or applications that make up functional compatible software is not acceptable under Making Tax Digital. For example, noting down details from an invoice in one ledger and then using that handwritten information to manually update another part of the business functional compatible software system.

A ‘digital link’ is one where a transfer or exchange of data is made, or can be made, electronically between software programs, products or applications. That is without the involvement or need for manual intervention such as the copying over of information by hand or the manual transposition of data between 2 or more pieces of software.

A digital link includes linked cells in spreadsheets, for example, if you have a formula in one sheet that mirrors the source’s value in another cell, then the cells are linked.

HMRC will also accept digital links as:

emailing a spreadsheet containing digital records to a tax agent so that the agent can import the data into their software to carry out a calculation (for instance, a Partial Exemption calculation)

transferring a set of digital records onto a portable device (for example, a pen drive, memory stick, flash drive) and physically giving this to an agent to import that data into their software

XML, CSV import and export, and download and upload of files

automated data transfer

API transfer

This list is not exhaustive.

HMRC does not consider the use of ‘cut and paste’ to select and move information, either within a software program or between software programs, to be a digital link.

3.2 .1.1 Soft landing regarding digital links requirements

HMRC will allow a period of time (‘the soft landing period’) for businesses to have in place digital links between all parts of their functional compatible software.

For the first year of mandation (VAT periods commencing between 1 April 2019 and 31 March 2020) businesses will not be required to have digital links between software programs. The one exception to this is where data is transferred, following preparation of the information required for the VAT Return, to another product (for example, a bridging product) that is API-enabled solely for the purpose of submitting the 9 Box VAT Return data to HMRC. The transfer of data to this product must be digital.

For the first year of mandation (VAT periods commencing between 1 April 2019 and 31 March 2020), where a digital link has not been established between software programs, HMRC will accept the use of cut and paste as being a digital link for these VAT periods.

The following rule has the force of law:

A digital link is an electronic or digital transfer or exchange of data between software programs, products or applications.

The use of ‘cut and paste’ does not constitute a digital link.

The following rule has the force of law:

If a set of software programs, products or applications are used as functional compatible software there must be a digital link between these pieces of software.

This digital link is required where the data to be included in any of the boxes of the VAT Return has been prepared within a software program, product or application, and this data is then transferred to another program, product or application in order to submit the VAT Return data to HMRC via the APIplatform.

For VAT periods starting on or after 1 April 2020, there must be a digital link for any transfer or exchange of data between software programs, products or applications used as functional compatible software.

3.2 .1.2 VAT calculations made outside of software

HMRC recognises that there may be points during preparation of your VAT Return when calculations will have to be made outside of any software you use to keep the digital records, or there may be a need to enter data into your software from particular sources. For example a capital goods scheme adjustment calculation done in a separate spreadsheet may need some form of input by hand into the software that will send your VAT Return information to HMRC.

3.2 .2 Submission of information to HMRC

The submission of information to HMRC must always be via an Application Programming Interface (API). While HMRC expects most businesses to use API-enabled commercial software packages both to keep digital records and file their VAT Returns, the following alternatives may be available.

3.2 .3 Bridging software

This is a digital tool (incorporating relevant Making Tax Digital APIs) that is used to connect accounting software to HMRC systems, and allows the required VAT information to be reported digitally to HMRC, and for information to be sent digitally back to the business from HMRC.

3.2 .3 .1 API-enabled spreadsheets

These are spreadsheets that incorporate relevant Making Tax Digital APIs. They can either:

combine with accounting software to submit the required VAT information digitally to HMRC, and allow information to be sent back to the business digitally from HMRC

be used to keep digital records and then directly submit the required VAT information digitally to HMRC

3.2 .4 Introducing the examples in section 7 of this notice

The examples in Section 7 include a number of examples of situations where a VAT registered entity is using a set of software programs with digital links that meet the requirements of Making Tax Digital. The examples also include situations where the transfer of data between programs does not need to be via a digital link as well as situations where a digital link is not mandatory for VAT periods starting before 1 April 2020.

3.3 Records that must be kept digitally

The records listed in the following paragraphs must be kept, maintained and preserved in digital form. The regulations refer to this information as your ‘electronic account’. The exact way you must enter the information will depend on the software package you have. Contact your software provider if you are unsure how to enter information into your software. HMRC can only provide advice on the legal requirements of Making Tax Digital.

You will need to keep additional records, such as invoices. You do not have to keep these digitally but you may choose to do so. For more information on the additional records that must be kept for VAT purposes, see VAT Notice 700/21: keeping VAT records.

3.3 .1 Designatory data

You must have a digital record of:

your business name

the address of your principal place of business

your VAT registration number

any VAT accounting schemes that you use

3.3 .2 Supplies made

For each supply you make you must record the:

time of supply (tax point)

value of the supply (net value excluding VAT)

rate of VAT charged

This only includes supplies recorded as part of your VAT Return. Supplies that do not go on the VAT Return do not need to be recorded in functional compatible software. For example intra-group supplies for a VAT group are not covered by these rules.

The time of supply is the date that you must declare output tax on. Typically this is when you send a VAT invoice or, if you are on cash accounting, when you receive payment for the supply. For more information on time of supply, see VAT Notice 700: VAT guide, section 14 and section 15.

Where more than one supply is recorded on an invoice and those supplies are within the same VAT period and are charged at the same rate of VAT you can record these as a single entry.

Example 1

You sold 10 standard rated items and 15 zero rated items on a single invoice then you would only need to record the total figures for each of the VAT rates.

Example 2

You are on standard accounting and a customer makes a part payment before you send out an invoice. If the payment and invoice were received and sent in the same period, you can record the supply as one transaction with one transaction date. Otherwise, where one supply needs to be recorded in different periods the precise manner will depend on the software. This could be done by splitting the amounts out, or the software may allow one line to show different periods for the VAT to be recorded.

You must also have a record of outputs value for the period split between standard rate, reduced rate, zero rate, exempt and supplies which are outside the scope of UK VAT. However, you only need to keep a digital record of ‘outside the scope’ supplies that you are required to include in your VAT Return.

For more information on completing your VAT Return, see VAT Notice 700/12.

The following rule has the force of law:

Where you need to apportion the output tax due on a mixed rate supply with a single inclusive price you do not have to record these supplies separately. You can record the total value and the total output tax due.

Not all software will allow you to record a rate of VAT other than the standard, reduced or zero/exempt. If this is the case, this mixed supply should be recorded as either one standard rated supply and one zero rated supply or you can record the sale at one rate and correct the VAT through an adjustment at the end of the period. You will also need to do this if you are using a margin scheme or the flat rate scheme.

Example 3

A business sells a meal deal for £3. It contains a zero rated sandwich, a standard rated pack of crisps and a standard rated drink. The apportionment shows that the VAT due is 30p. The business can record this as an individual supply with 30p of output tax if their software allows this. Below are 3 potential ways this could be recorded.

(i) Software allows input of total VAT

The value of the supply (net value excluding VAT) £2.70

Total VAT charged: £0.30

(ii) Meal deal recorded as standard rated and zero rated supplies

If their software does not allow this they could record the supply as a standard rate element of £1.50 and a zero rated element of £1.20.

Element 1 (standard rated portion)

The value (net value excluding VAT) £1.50

The rate of VAT charged: Standard rate

Element 2 (zero rated portion)

The value (net value excluding VAT) £1.20

The rate of VAT charged: Zero rate

(iii) Supply recorded at one rate and VAT corrected at the end of the period

Alternatively, they could record the meal deal as one entry and correct the VAT at the end of the period.

The value of the supply (net value excluding VAT) £2.70

The rate of VAT charged: Standard rate

Adjustment to correct mixed rate VAT: -£0.24

3.3 .2.1 Supplies made by third party agents

A third party agent can act for, or represent, a business in arranging supplies of goods or services. The supplies that you arrange are made by, or to, the business represented.

HMRC is aware of a number of circumstances in which a third party agent makes supplies on behalf of a business and it may not be possible or practical for the business to record digitally every single supply. Therefore HMRC can accept businesses recording these digitally as a single invoice.

The following rule has the force of law:

Where a third party agent makes supplies on your behalf, those supplies do not fall within the digital record keeping requirements until you receive the information from the agent. Where the information is received as a summary document you can treat this document as one invoice issued by you for the purpose of creating your digital record.

This relaxation only varies the requirements on maintaining records using functional compatible software. It does not change any other record keeping requirements set out in VAT legislation.

Further information on supplies made by or through agents can be found in VAT Notice 700: VAT guide, section 22 to section 25.

Example 4

A business uses a letting agent to rent out a number of properties. Each month the letting agent provides a summary of the rents collected and VAT charged. The business can treat all supplies covered in this summary document as if they were covered by a single sales invoice, rather than treating each invoice issued on their behalf separately. They can group transactions together providing they are within the same VAT period and are charged at the same rate of VAT.

This rule would not cover circumstances where responsibility for supplies is assumed by other persons who are not third party agents of the business. For example it does not cover supplies made by an employee on behalf of your business or by a charity volunteer for the purposes of a fundraising event such as a church fete.

3.3 .3 Supplies received

For each supply you receive you must record the:

time of supply (tax point)

value of the supply

amount of input tax that you will claim

This only includes supplies recorded as part of your VAT Return, supplies that do not go on the VAT Return do not need to be recorded in functional compatible software. For example, wages paid to an employee would not be covered by these rules.

There is no requirement under the regulations to record inputs for the period split by VAT rate.

The time of supply is typically the date on the VAT invoice or, if you are on cash accounting, when you pay for the supply. However you must also hold the associated evidence to claim deduction of input tax. For more information on time of supply, see VAT Notice 700: VAT guide, section 14 and section 15 and also paragraph 10.5 of that same Notice for information on timescales for claiming input tax.

If more than one supply is on an invoice you can record the totals from the invoice. Where the amount of input tax that you will claim is not known at the time you record the supply you have received, you can record:

the total amount of VAT and adjust for any irrecoverable VAT once calculated

no VAT and adjust for any recoverable VAT once calculated

VAT recoverable based on an estimated percentage and adjust for any VAT once calculated

See paragraph 3.4 of this Notice for information on adjustments.

Where an invoice includes supplies with different times of supply that are within the same VAT period, you may record all supplies on the invoice as being at the same date.

Example 1

A business uses cash accounting and has paid the amounts on the invoice over 3 months. Two of the months are in the same VAT period so can be recorded together. The payments relating to the other month must be recorded separately. The precise manner of recording the information in different periods will depend on the software. This could be done by splitting the amounts out, or the software may allow one line to show different periods for the VAT to be recorded.

If a business pays the actual cost or a proportion of the travel and subsistence cost of an employee, it can claim the total or a proportion of the total input tax incurred.

The following rule has the force of law:

Where you are claiming input tax on employee expenses and your employee provides the combined value of more than one purchase, you do not have to record each purchase separately. You can record the total value and the total input tax due.

Further information on subsistence and the effect on input tax claims can be found in VAT Notice 700: VAT guide, section 12.

3.3 .3.1 Supplies received by third party agents

A third party agent can act for, or represent, a business in arranging supplies of goods or services. The supplies that you arrange are made by, or to, the business represented.

HMRC is aware of a number of circumstances in which a third party agent makes purchases on behalf of a business and it may not be possible or practical for them to record digitally every single supply received. Therefore HMRC can accept businesses recording these digitally as a single invoice.

The following rule has the force of law:

Where a third party agent makes purchases on your behalf, those purchases do not fall within the digital record keeping requirements until you receive the information from the agent. Where the information is received as a summary document you can treat this document as one invoice received by you for the purpose of creating your digital record.

This relaxation only varies the requirements on maintaining records using functional compatible software. It does not change any other record keeping requirements set out in VAT legislation.

Further information on supplies made by or through agents can be found in VAT Notice 700: VAT guide, section 22 to section 25.

3.3 .4 Reverse charge transactions

If your software records reverse charge transactions you do not need separate entries for the self supply and purchase. If your software does not record reverse charge transactions you will need to record reverse charge transactions twice, once as a supply made and a second time as a supply received.

For information on reverse charge transactions see VAT Notice 741A: VAT place of supply of services, section 5.

3.3 .5 Summary data

To support each VAT Return you make, your functional compatible software must contain:

the total output tax you owe on sales

the total tax you owe on acquisitions from other EU member states

the total tax you are required to pay on behalf of your supplier under a reverse charge procedure

the total input tax you are entitled to claim on business purchases

the total input tax allowable on acquisitions from other EU member states

the total tax that needs to be paid or you are entitled to reclaim following a correction or error adjustment, and

any other adjustment allowed or required by VAT rules

A total of each type of adjustment must be recorded as a separate line.

3.4 Adjustments

Where you are allowed or required to adjust the input tax claimed or output tax you owe according to the VAT rules you must record this adjustment in functional compatible software. Only the total for each type of adjustment will be required to be kept in functional compatible software, not details of the calculations underlying them.

If the adjustment requires a calculation, this calculation does not have to be made in functional compatible software. If the calculation is completed outside of functional compatible software then digital links are not required for any information used in the calculation. However using software for all your calculations will reduce the risk of errors in your returns.

The following rule has the force of law:

Where the input tax claimed or output tax due on a supply has been changed as the result of an adjustment you do not need to amend the digital record of the supply.

Example 1

A partly exempt business software allows it to record amounts of VAT relating to both exempt and taxable supplies. At the end of the period they complete a partial exemption calculation and put the adjustment into their return. The calculation is not completed in the software. The business does not have to go back and change each line in the software to reflect the amount of recovery on each invoice.

Example 2

A business has a software package that requires a period to be closed before the return can be completed. After the period has been closed the business is calculating adjustments before submitting the return. Invoices are found that should be included on the return. The business can enter the figures as an adjustment to ensure the return is correct, but they must record the invoices in their functional compatible software to complete their digital records.

This relaxation only varies the requirements on maintaining records using functional compatible software. It does not change any other record keeping requirements set out in VAT legislation.

Where a business makes an error correction using method 2, they are not required to amend the input tax claimed or output tax charged recorded in the digital record of the supply.

Example 3

A business notices an error in its records. The total value of the error is £65,000 so the business must correct the error using error correction method 2. The business does not have to make any changes in its functional compatible software, but must keep all records as normal.

This relaxation only varies the requirements on maintaining records using functional compatible software. It does not change any other record keeping requirements set out in VAT legislation.

3.5 Retail schemes

The following rule has the force of law:

In addition to the records listed in paragraph 3.3 above, if you account for VAT using a retail scheme you must keep a digital record of your Daily Gross Takings (DGT). You are not required to keep a separate record of the supplies that make up your DGT within functional compatible software.

If you account for VAT using the Flat Rate Scheme:

you do not need to keep a digital record of your purchases unless they are capital expenditure goods on which input tax can be claimed

you do not need to keep a digital record of the relevant goods used to determine if you need to apply the limited cost business rate

If your software does not include a Flat Rate Scheme setting, and does not allow you to include a rate of VAT other than standard, reduced, zero/exempt, then you will need to record the supply as either one standard rated supply and one zero rated supply. Alternatively, you can record the sale at one rate and correct the VAT through an adjustment at the end of the period, using the same method HMRC will allow you to use to correct the VAT on a mixed supply (see paragraph 3.3.2 above).Further information on the Flat Rate Scheme can be found in VAT Notice 733: Flat Rate Scheme for small businesses.

3.7 Gold Special Accounting Scheme

The following rule has the force of law:

In addition to the records listed in paragraph 3.3 above, if you make any sales under the Gold Special Accounting Scheme, you must keep a digital record of the following:

value of sales made under the special accounting scheme for gold

total output tax on purchases under the special accounting scheme for gold

3.8 Margin schemes

You are not required to keep the additional records required for these schemes in digital form, nor are you required to keep the calculation of the marginal VAT charged in digital form. These records must still be maintained in some format.

If you do keep a digital record and your software does not allow you to record the VAT on the margin, then you will need to record the supply as either one standard rated supply and one zero rated supply. Alternatively, you can record the sale at one rate and correct the VAT through an adjustment at the end of the period, using the same method HMRC will allow you to use to correct the VAT on a mixed supply (see paragraph 3.3.2above).

VAT updates is a feature of Making Tax Digital that will be available at a future date. They will allow businesses to provide VAT information to HMRC outside of a VAT Return voluntarily. A VAT update will not include different information to that submitted in a VAT Return. Further information and detail about this functionality will be published in due course.

5 Supplementary data

Supplementary data is a feature of Making Tax Digital that will be available at a future date. It will be voluntary. HMRC will specify what supplementary data will be, but broadly this will be information that supports the 9 box VAT Return that is the summary data described in paragraph 3.3.5 above. You will be able to submit supplementary data each time you submit a voluntary VAT update or VAT Return. Further information and detail about this functionality will be published in due course.

6 Agents

You may authorise HMRC to receive data from (and send data to) an agent on your behalf in relation to any Making Tax Digital service. Once you have done this, that agent can sign up your business to that service, and use software to create, view, edit and send your data to HMRC. Your agent may also keep and maintain digital records on your behalf. If you have previously authorised HMRC to receive your VAT Return from an agent they can still do this. Agents will not need to be re-authorised by their clients to act for them in the Making Tax Digital VAT service where they already have existing authorisation to act for VAT purposes.

You will be able to have more than one agent if you wish, performing different Making Tax Digital services for you, and you will be able to manage different levels of permission for each of them.

Agents will need to sign up to a new agent services account to use Making Tax Digital services on behalf of their clients. The agent must have software of their own or have access to the software that holds your digital records.

Agents will not necessarily have access to all of your source data so, for example, they may not always be able to make corrections to your digital records. In these circumstances your agent will need to advise you of any corrections required to those digital records.

HMRC will provide access to taxpayer information we hold, and the necessary services, only to those agents who have been properly authorised.

7 Examples of where a ‘digital link’ is required

The examples set out here are intended to illustrate the extent to which a digital link is required between programs within a set of software programs used by a business or its agent. They show where information transfer must be digital and where it need not be, taking into account the variety of digital record keeping and reporting options that businesses will have.

These scenarios are not intended to be exhaustive or prescriptive; they merely illustrate the more common ones.

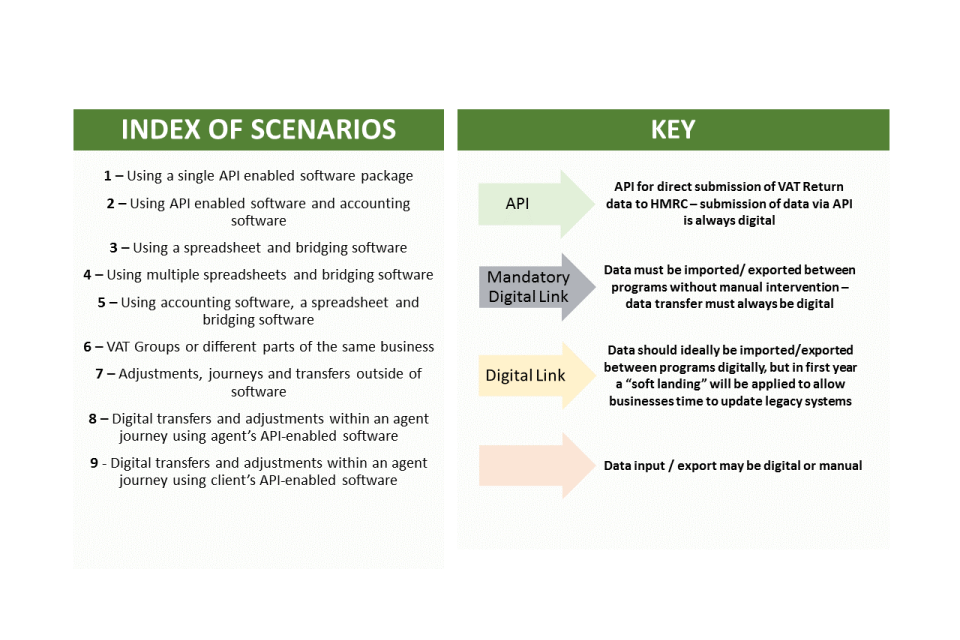

The image below contains the index of scenarios for:

using a single API-enabled software package

using API-enabled software and accounting software

using a spreadsheet and bridging software

using multiple spreadsheets and bridging software

using accounting software, a spreadsheet and bridging software

VAT groups or different parts of the same business

adjustments, journeys and transfers outside of software

digital transfers and adjustments within an agent journey using agent’s API-enabled software

digital transfers and adjustments within an agent journey using client’s API-enabled software

The image also contains a key for:

API – API for direct submission of VAT Return data to HMRC – submission of data via API is always digital

mandatory digital link – data must be imported or exported between programs without manual intervention – data transfer must always be digital

digital link – data should ideally be imported or exported between programs digitally, but in first year a ‘soft landing’ will be applied to allow businesses time to update legacy systems

data input or export may be digital or manual

Example 1 – Using a single API-enabled software package

The image below describes a business that uses a single functional compatible software package.

It uses a single software product to record all sales, purchases, and expenses in a digital format. The software has the necessary functionality to maintain the mandatory digital records, prepare the VAT Return, and submit this to HMRC via an API. In this situation, all data transfer must be digital.

Example 2 – Using API-enabled software and accounting software

The image below describes a business that uses accounting software and API-enabled software.

It uses the accounting software to record all sales, purchases, and expenses in a digital format, and then transfers the totals for each of these to API-enabled software which prepares the VAT Return. The API-enabled software has the necessary functionality to maintain the mandatory digital records, prepare the VAT Return, and submit this to HMRC via an API.

During the soft landing period, HMRC will not require a digital link between the accounting software and the API-enabled software. However, for VAT periods commencing from 1 April 2020, there must be a digital link between the software.

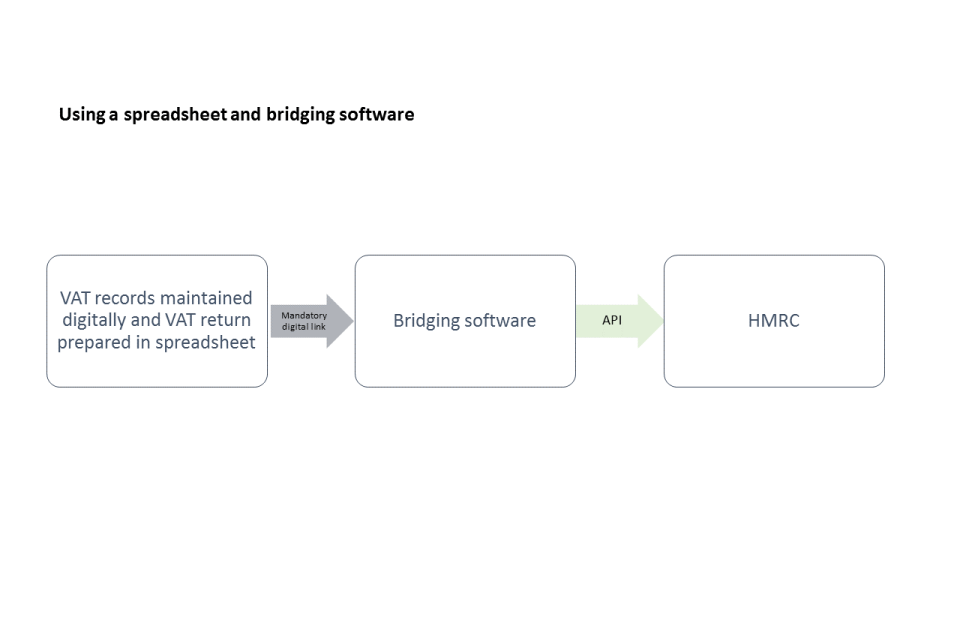

Example 3 – Using a spreadsheet and bridging software

The image below describes a business that uses a spreadsheet and bridging software from April 2019, which allows the information to be transferred to HMRC via an API.

It uses a spreadsheet to record all sales, purchases, and expenses in a digital format. The VAT Return is then prepared within the spreadsheet, using formulae already written into the spreadsheet.

The VAT Return information is then sent via a mandatory digital link to bridging software, which digitally submits the information directly to HMRC.

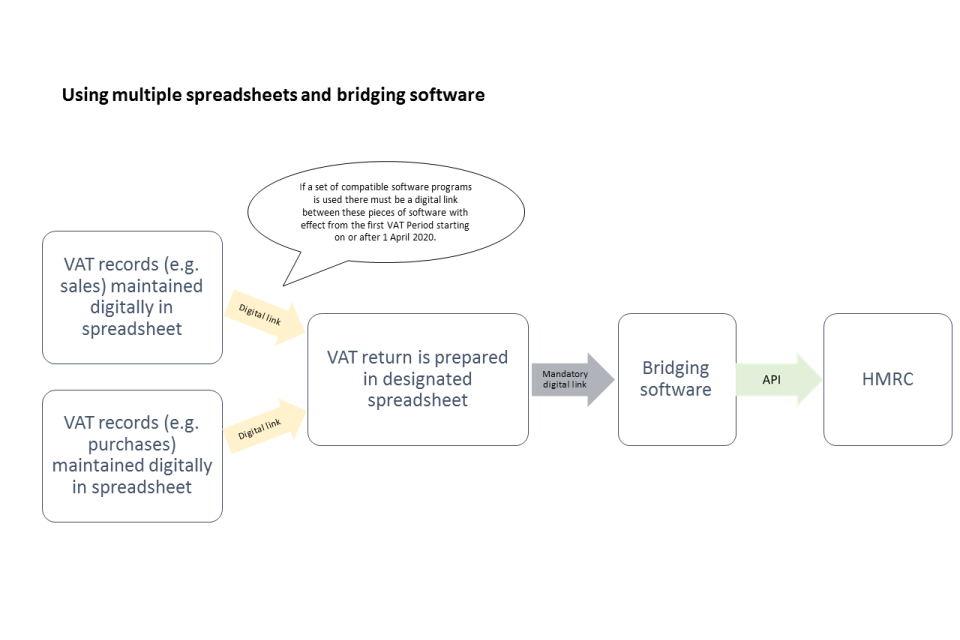

Example 4 – Using multiple spreadsheets and bridging software

The image below describes a business that uses more than one spreadsheet, linked to bridging software.

A business uses 2 spreadsheets to record sales, purchases, and expenses in a digital format. A third and final spreadsheet is designed to receive information from the record keeping spreadsheets and prepare the VAT Return. This final spreadsheet is digitally linked to bridging software, which submits the VAT Return to HMRC via an API. (As an alternative to bridging software, the final spreadsheet could have API functionality built into it.)

During the soft landing period, HMRC will not require the spreadsheets that supply the relevant data for the final spreadsheet to have a digital link. However, for VAT periods commencing from 1 April 2020, there must be digital links to the final spreadsheet.

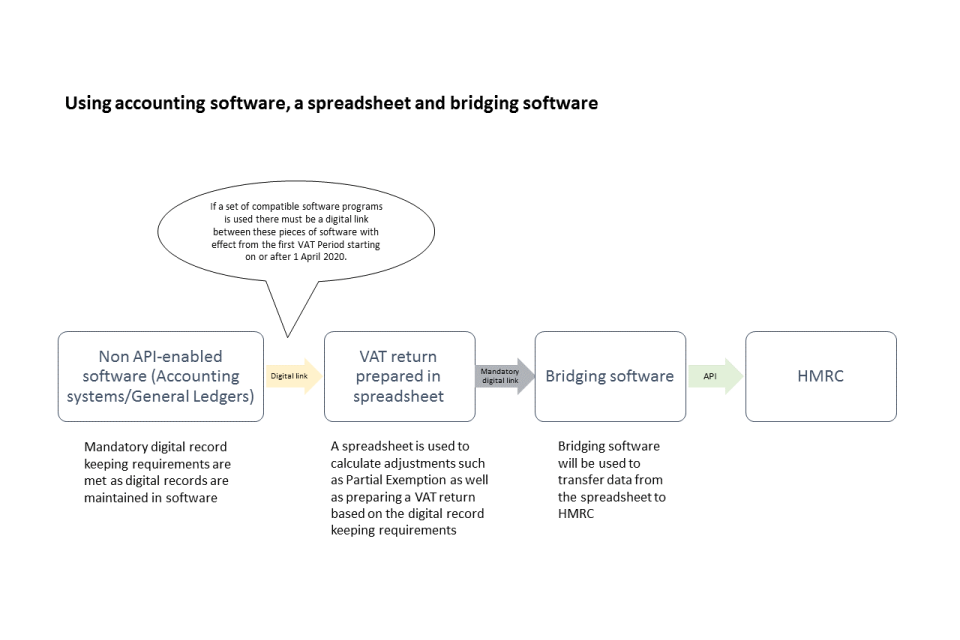

Example 5 – Using accounting software, a spreadsheet and bridging software

The image below describes a business that uses 3 pieces of software:

spreadsheets

accounting software

bridging software

It uses accounting systems or general ledgers (which are not API-enabled) to record all sales, purchases, and expenses in a digital format, and then transfers the totals of each of these into a spreadsheet used to prepare the VAT Return. This spreadsheet may also be used for any Partial Exemption calculation that is required. The return information in the spreadsheet is then sent via a mandatory digital link to bridging software, which submits the VAT Return to HMRC via an API. (As an alternative to bridging software, the spreadsheet could have API functionality built into it.)

Altogether the 3 separate pieces of software maintain the digital electronic records required by the regulations, prepare the return and submit it to HMRC. During the soft landing period between 1 April 2019 and 31 March 2020, HMRC will not require a digital link to exist between the non-API-enabled software and the spreadsheet. However, all information must be transferred between software programs using a digital link for VAT periods commencing from 1 April 2020.

Example 6 – VAT groups or different parts of the same business

The image below describes VAT groups or different parts of the same business where each member of the VAT group (or different area of a business with a single VAT registration) uses their own software to keep and maintain digital records. This might include a local authority, a farming business with a separate farm shop or B&B, or a large estate. The group or business uses one spreadsheet to prepare the VAT Return information and bridging software.

Each group member’s software calculates the required information needed for their part of the VAT Return. Each group member’s software then sends this information by a digital link, to a spreadsheet which is used to compile the totals for the group and prepare the VAT Return for the whole of the group. The return information in the spreadsheet is then sent via a mandatory digital link to bridging software, which submits the VAT Return to HMRC via an API. (As an alternative to bridging software, the spreadsheet could have API functionality built into it.)

Together, the separate pieces of software maintain the digital records required by the regulations, prepare the VAT Return and submit the return to HMRC.

During the soft landing period between 1 April 2019 and 31 March 2020, HMRC will not require a digital link to exist between each group member’s software and the spreadsheet. However, the links between the pieces of software must be digital from 1 April 2020 for the set of software to be considered functional compatible software for Making Tax Digital purposes. While HMRC expects that each group member will operate digital links within the software that it uses, it does not expect the software systems of each group member to be linked to other group members’ software systems for VAT purposes if there is no need for them to transfer 9 box VAT Return information between the members.

Example 7 – Adjustments, journeys and transfers outside of software

The image below describes a business that uses API-enabled accounting software and spreadsheets.

It uses the API-enabled accounting software to record all sales, and purchases, and expenses in a digital format. This software is able to prepare the VAT Return. However, the business uses a spreadsheet to calculate adjustments such as a partial exemption calculation or working out road fuel scale charges. Information from the API-enabled software such as inputs, outputs and totals, is transferred to the spreadsheet either via a digital link or by manual transfer. The spreadsheet uses this data to calculate any adjustments, and these adjustments are transferred back into the API-enabled accounting software, which calculates and submits the VAT Return.

As the calculations in the spreadsheet are not required to be kept digitally in functional compatible software, the business can type the adjusted figures into its API accounting software. However, using a digital link for these processes, rather than a manual transfer, reduces the chance of errors.

Example 8 – Digital transfers and adjustments within an agent journey using agent’s API-enabled software

The image below describes a business that uses accounting software and employs an agent to prepare and submit its VAT Return using the agent’s API-enabled software.

The business uses accounting software to record all sales, purchases, and expenses in a digital format. It transfers this information to the agent through a link which must be digital for VAT periods commencing from 1 April 2020.

Once the data is transferred, the agent uses their API-enabled software to prepare the VAT Return for the business. Any amendments that are made outside of the agent’s software (for instance, in a spreadsheet), from correcting mistakes to adjustments required by VAT law, is entered into the agent’s functional compatible software. These amendments are part of the required digital records. This means these changes must be either recorded in the client’s records or the agent must store the changes and allow the client can access to the records. The agent’s software then prepares the VAT Return and submits this to HMRC via an API.

As the adjustments made outside of the agent’s software are not required to be kept digitally in functional compatible software, the agent can type the adjustment into their accounting software. However, using a digital link for these processes, rather than a manual transfer reduces the chance of errors.

Example 9 – Digital transfers and adjustments within an agent journey using business’ API-enabled software

The image below describes a business that uses a single functional compatible software package but also uses an agent to calculate adjustments, which the agent does using its own software.

The business uses its software package to keep its digital records and prepare and submit the VAT Return. It gives the agent access to its software. Depending on the needs of the business, agents may be given access to either the client’s full set of information or only be given a limited view. The agent selects the necessary data to enable it to make adjustments in its own software.

Any corrections or amendments must be reflected in the client’s digital records. Adjustments may be made in the business’ software by the agent manually. However using a digital link to transfer the information will reduce the chance of errors. Once amendments have been fed back into the VAT Return, the return is digitally submitted from the business’ software to HMRC via an API.

Together, all the software described above (business’ software and agent’s software) maintain digital records as required by the regulations, prepare the VAT Return and submit the return to HMRC.

Businesses will not be mandated to use Making Tax Digital until April 2019 and then only for those above the VAT threshold.

In April 2018, simple VAT-registered entities were invited to join the pilot programme.

Interested parties have time to pause and aim for a more achievable implementation date.

HMRC has published a VAT guide, stakeholders’ communication pack and list of software suppliers.

Bridging software that will enable data to be taken from spreadsheets and converted into an MTD-friendly format is becoming available.

The government will not widen MTD before April 2020 at the earliest.

What? A minister who listens? It’s a little over a year ago since the then recently-appointed Financial Secretary to the Treasury, Mel Stride, published a written statement (tinyurl.com/HMT-7423) responding to disquiet about the proposals for Making Tax Digital (MTD). This said: ‘Having listened carefully to the concerns raised by the Treasury Select Committee, parliamentarians and stakeholders, the government is announcing policy changes that will be reflected in the legislation to be introduced.’

He continued: ‘Businesses will not be mandated to use the Making Tax Digital system until April 2019 and then only to meet VAT obligations. This will apply to businesses with a turnover above the VAT threshold. Businesses with turnover below the VAT threshold will not be required to use the system but can choose to do so. Businesses will also be able opt in for other taxes, benefiting from a streamlined, digital experience.’

Mr Stride’s action was a commonsense move born out of a series of delays that had beset the rollout of MTD. These dated from when George Osborne announced ‘the death of the tax return’ in his March 2015 Budget speech although, I hasten to add, they were not of HMRC’s making.

Impact of the announcement

The effect of this about-face was equivalent to a release of pressure from a safety value. All parties could pause, regroup and aim for the more achievable April 2019 target with a much-reduced administrative burden.

Although income tax mandation for the self-employed and unincorporated landlords (hereafter both referred to as the self-employed) might be off the table in the short term, HMRC promised to continue working with software developers along its original delivery roadmap. The aim was to ensure that MTD-compliant products from third parties would be available for those wishing to join the new income tax pilot.

What happened next?

In response, almost all software companies redeployed their internal development resources away from attempting to meet the demands of HMRC’s MTD income tax quarterly filing requirement to ensuring delivery of the more straightforward VAT-MTD compliant products well ahead of April 2019 VAT mandation.

At the end of October 2017, HMRC released the application programming interfaces (APIs) required to transmit to HMRC all the data contained in nine boxes of information and the associated declaration that make up a traditional VAT return.

An API is, in effect, the virtual plumbing (programming) required to connect third-party software to HMRC’s platform so that data can be transmitted to and received from it. This is in much the same way as banking apps on a smartphone can send and retrieve data from a bank’s back-end system.

In November, HMRC began to accept the transmission of technical data (test data) from developers as a way of testing that the VAT APIs embedded into their software worked.

Then, in early April 2018 and without a fanfare, HMRC invited VAT-registered entities with the simplest of affairs to sign up to join its MTD-VAT pilot. On 26 April, it released the APIs that developers required to enable their software to transmit live data straight to HMRC’s enterprise tax management platform (ETMP).

Soon afterwards, HMRC received the first MTD-compliant VAT submission.

As MTD is rolled out and more heads of duty are moved on to HMRC’s EMTP, taxpayers will be able see their complete financial picture through their digital account, just as they do in online banking. In the longer term, HMRC’s publication Making Tax Digital for Business: VAT Guide for Vendors states: ‘They will be able to set an over-payment of one tax against the under-payment of another. It will feel like paying a single tax.’ (See here)

Private testing

Although it may be accepting live data, VAT-MTD is in a controlled period of testing – known as a private beta testing phase. Only applicants with simple VAT affairs that meet HMRC’s initial tight admission criteria are accepted into this live pilot.

It is likely that the MTD-VAT pilot has significantly fewer than 500 VAT-registered entities taking part now. However, assuming all goes well HMRC will gradually relax its selection criteria, thus permitting a greater range of entities to join.

Latest developments

On 13 July, HMRC published:

an MTD VAT guide (VAT Notice 700/22: Making Tax Digital for VAT);

an HMRC communication pack for stakeholders; and

a list of software suppliers supporting Making Tax Digital.

With about eight months to VAT mandation, pressure from commentators to compel HMRC to publish its MTD VAT guide had been ramping up. Not least because guidance was required to clarify what constituted digital record-keeping, what was meant by functionally compatible software and what digital links looked like.

At point 3.2.1.1, the guide covers the post-April 2019 one-year penalty soft landing for those mandated to join next year but who will be unable to establish digital links between one piece of accounting software and another in time.

Many stakeholders, such as trade bodies and software suppliers, had been pressing HMRC to publish the communications pack to provide information and source material so that they in turn could inform their stakeholders.

The publication of the software supplier list allows those advising on or faced with complying with the April 2019 VAT mandation to gain a level of reassurance that large third-party software solution providers such as Intuit have market-ready, VAT-MTD compliant software.

Bridging software

From an MTD perspective, bridging software is a third-party, API-enabled software product capable of drawing data digitally from a spreadsheet, turning it into a format compatible with MTD for VAT and then validating it before submitting the information to HMRC at the touch of a button.

Until recently, this long-promised piece of software had been assuming the mythical status accorded to the likes of the Loch Ness Monster – in other words, everyone has heard of it, everyone has a view of what it would look like but … no one had actually seen it.

All that is changing. BTC Software and PwC have recently announced they have market-ready bridging products. What’s more, PwC plans to make its product free to charities that might otherwise struggle to meet the cost of complying with HMRC’s VAT-MTD requirements.

Expect others to follow…

The great thing about bridging software is that it promises an affordable way for VAT-registered entities, such as spreadsheet users, to comply with HMRC’s MTD digital end-to-end requirement. It also affords businesses of significant size, often with disparate systems that do not speak to one another or groups with non-integrated accounting, the same opportunity.

What bridging software does not do is provide the level of added-value functionality, such as near limitless management reports, built in as standard to third-party, cloud-based accounting packages.

So where are we now?

There are just over 20 developers with VAT-MTD-ready products. Further, HMRC has stated that more than 150 software suppliers have registered an interest in providing software for VAT-MTD. Of those, more than 40 have said they will have software ready during the private beta phase of the VAT-MTD pilot. (See here.)

All this, combined with the filing of MTD-compliant VAT returns during the private beta period puts the department in a much better place to deliver VAT-MTD than it was immediately before Mr Stride’s announcement. That said, I see the position as finely balanced. We are less than eight months away from mandation and it does not look like VAT-MTD will emerge from its private beta phase anytime soon.

At the end of June, the British Chamber of Commerce called for a postponement to ‘allow the Revenue to focus its immediate attention on supporting businesses through the Brexit process, which must be a key priority’. Others, like myself, remain more optimistic.

However, a limited number and type of VAT-registered entities are engaged in private beta testing and there is no clear indication of when the public beta phase will start. Consequently, there will come a point soon – and certainly before the end of the summer (before the middle of October in Civil Service speak) – when HMRC will need to give serious consideration to extending the pilot testing phase by deferring the mandation start date.

A glance into the future

Further into his July 17 written statement Mr Stride wrote: ‘The government will not widen the scope of MTD beyond VAT before the system has been shown to work well, and not before April 2020 at the earliest. This will ensure that there is time to test the system fully and for digital record-keeping to become more widespread.’

Given the limited scope of the VAT-pilot and that VAT mandation is just over eight months away, I believe there is insufficient time, using the minister’s own words, ‘to test the system fully and for digital record-keeping to become widespread’ to garner the evidence required to support an earlier extension to mandation.

As well as this, and for the reasons stated earlier, there is not the income tax MTD-compliant third-party software products available (HMRC has a list of four). This situation looks unlikely to change until VAT-MTD is successfully delivered and the software industry is reassured that ministers have an appetite for mandation. Experience suggests that, once an announcement about mandation is made, it will change quickly as developers move quickly to capitalise on the opportunity.

Despite being a passionate believer in what MTD has to offer, and that the future of the accountancy profession is in the cloud, I cannot see further mandation returning to the table before 2021 at the very earliest. In the meantime, ministers and HMRC must contend with that other small cloud on the political horizon … the travails of Brexit.